Justine Simpson, Leeds Beckett University, UK

Authentic learning provides a learning environment which gives students a taste of the real world. It requires students to be given the opportunities to undertake the kind of tasks that would be carried out in the workplace and means that theoretical knowledge is applied to scenarios which are akin to those found in reality. To quote Aristotle (2004), “For the things we have to learn before we can do them, we learn by doing them.” Learning by doing is thought to be one of the most effective ways to learn (Lombardi, 2007).

With developments in technology, the internet and software applications it is now easier than ever to offer students authentic learning environments covering a wide range of applications offering solutions such as real world simulations, entering data onto software packages as used in the work place, film clips and internet based products.

This paper aims to establish whether by introducing authentic learning into the Masters in Business Administration (MBA) module Accounting and Finance for Decision Making, ‘learning by doing’ is more effective in terms of pass rates, by measuring whether they have improved with the introduction of authentic learning activities and assessment methods and also whether students enjoy the experience of learning ‘authentically’ by measuring student satisfaction before and after the changes to the learning environment. Prior to this study, the module was delivered in a very theoretical way with minimal use of authentic learning techniques.

This paper will focus on measuring the success of introducing authentic learning methods into the finance part of the Accounting for Decision Making module taught as part of the MBA programme.

The reason for choosing this specific module is that this MBA module has a large number of overseas students as participants who often struggle with their English language skills, especially because the subject uses a lot of technical terminology. Module evaluation suggested that students did not enjoy the subject. It also had poor pass rates with a large number of students re-sitting it each semester over the last three years.

The module had been taught historically by the students receiving lots of factual information via PowerPoint presentations in one hour lectures backed up by exam-style question practice in one and a half hour seminars. The exam-style questions were very technical with little room for discussion of the material and no application of their use in the real world. However, the style of the questions mirrored the format of the questions set in the summative exam. As a result there was little interaction in the classroom between students and the tutor and little appreciation of the relevance of topics taught to the type of decision making the subjects were applicable to in business situations. Topics within the module cover areas such as ‘sources of finance’ which if just taught as a list of sources available for businesses to fund their activities by can be easily forgotten and not appreciated in terms of which source of finance is most appropriate for alternative projects and businesses.

This traditional style of module teaching did little to retain interest and enjoyment for the students and did not highlight the importance and relevance of topics to decision making in businesses. Issues to be considered were the restrictive style of teaching, learning and assessment and how the incorporation of technology and more authentic style scenarios could enhance learning, enjoyment and assessment and hopefully improve pass rates. More authentic learning should be more enjoyable for both students and staff involved in the module.

The traditional style of delivery used mirrored the style of questioning in the summative assessment. However, formal lectures and exam style written questions involving calculations and brief narrative to check knowledge in seminars is quite hard and dry and particularly difficult for overseas students to grasp the technical nature and understanding of the subject. In addition, according to the work of Fleming (2001), there are a number of styles of learning which students can adopt namely visual, auditory, reading/writing and kinaesthetic (Leite, Svinicki, & Shi, 2009). If just one style of learning is used this may limit a large proportion of students in the classroom in terms of their learning.

A variety of questions need to be considered when introducing changes to teaching styles such as what range of learning activities would be appropriate for the subject as well as the students? How do we know whether the methods used are authentic? Have employers, graduate recruiters, professional bodies, etc. been consulted? Is there a good balance of activities – not more of the same kind?

This section reviews how relevant literature defines what authentic learning is and the tools and techniques which can be used as part of it. It mainly focuses on explaining some of the work by Herrington (2006) and Lombardi (2007). As the aim of the study is to use authentic learning techniques to improve pass rates and the enjoyment of student learning, it also tries to review literature on authentic learning in terms of its suggested link with effective learning and student enjoyment.

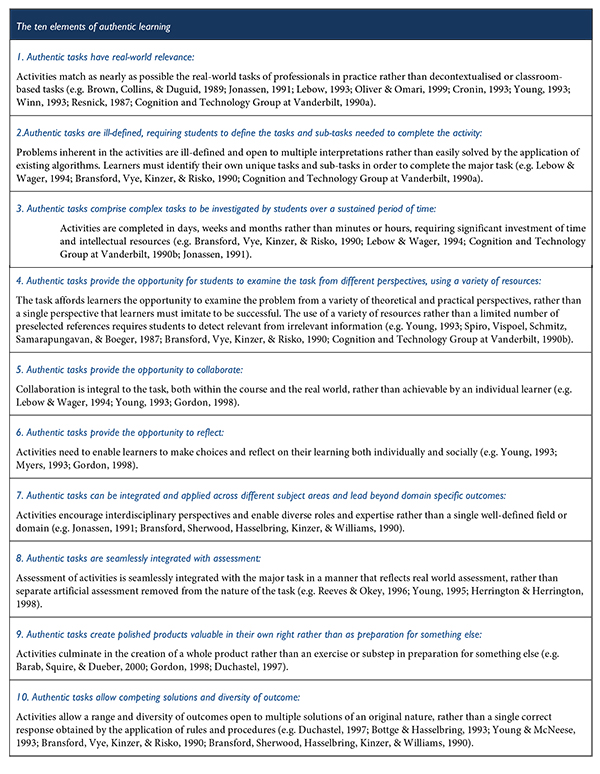

According to the White Paper ‘Authentic Learning for the 21st Century; An Overview,’ Lombardi (2007) defines authentic learning as typically focusing on real-world, complex problems and their solutions, using role-playing exercises, problem-based activities, case studies, and participation in virtual communities of practice. Lombardi’s work summarises authentic learning into ten elements “providing educators with a useful checklist that can be adapted to any subject matter domain” (Lombardi, 2007, p. 3).

These ten authentic learning design elements are real-world relevance, ill-defined problem, sustained investigation, multiple sources and perspectives, collaboration, reflection, interdisciplinary perspective, integrated assessment, polished products and multiple interpretations and outcomes (Lombardi, 2007, pp. 2-4). These are expanded on in detail in table 1 taken from the work done by Herrington (2006):

Table 1: Herrington, 2006, p. 5

The introduction of authentic learning into higher education began in the late 1980s. According to Herrington (2006), two papers established the context of the importance of authentic learning in higher education. These were by Brown, Collins, and Duguid (1989) and Collins, Brown, and Newman (1989). Collins et al. (1989, p. 2) state that authentic learning is “the notion of learning knowledge and skills in contexts that reflect the way the knowledge will be useful in real life’’.

Further exploration then continued in the 1990s by Reeves and Reeves (1997), Honebein, Duffy, and Fishman (1993), Lebow and Wager (1994) and Chambers and Stacey (1999), who focused on the central function of an authentic task. This research in the 1980s and 1990s then led to the summary of the findings into the ten elements listed above in the 2000s, which were used as criteria on which to base authentic learning activities.

The ten elements detailed above can be interpreted as meaning that authentic activities are concerned with what would be carried out in the real world by relevant professionals and consist of challenging problems which take time to evaluate. In carrying out the activity, different resources can be consulted, students need to work collectively, reflect, use different disciplines and ideally follow a number of tasks woven into one major one which has value in its own right. Finally, to be authentic the activity also needs to be open to interpretation and have a number of solutions.

To achieve all of these elements in one activity would be very difficult therefore the list implies that a number of activities woven into one major one would be a suitable way to introduce authentic learning into the classroom. For example, one exercise could encourage students to work together on a real-world simulation, another could involve them working individually reflecting on their learning experience.

An over-riding emphasis seems to be on authentic activities reflecting the ‘real world’ but to achieve a number of the elements above, the way these are integrated into the learning environment would need to be quite varied and may cause issues as to what is the most appropriate tool to use for certain subjects.

Lombardi also states that, “educational researchers have found that students involved in authentic learning are motivated to persevere despite initial disorientation or frustration, as long as the exercise simulates what really counts,” (Lombardi, 2007, p. 4). This implies that using authentic learning techniques can be more motivating for students to study who may struggle with more traditional methods as is appropriate for the module being reviewed here, however the fact that the exercise “simulates what really counts” is quite vague and may be open to interpretation in different contexts. For example, how does a student know what really counts when they may have no work experience and how may an academic reassure them when they have not worked in the ‘real world’ for a number of years?

The consideration of authentic learning tends to be perceived as a relatively new concept, however apprenticeships and learning a trade have been in existence for hundreds of years and these are first and foremost ways of learning by doing. In higher education, learning has traditionally been more technical and academic but there is no reason teaching methods cannot incorporate more practical and varied techniques to assist learning. Certainly, technology has a big part to play in the enabling of more ‘real world’, practical methods of learning to take place in the classroom. Technology can establish simulations, store data, enable modelling and a whole host of other tools to be incorporated as outlined in the ten design elements listed above. In addition, multiple sources, collaboration, integrated assessment, defining problems are all possible through IT tools.

Lombardi conveniently summarises how technology can support authentic learning environments as detailed below:

High-speed internet connectivity for provision of multimedia information, including dynamic data and practical visualisations of complex phenomena and access to remote instrumentation in conjunction with expert advice.

Asynchronous and synchronous communication and social networking tools for the support of teamwork, including collaborative online investigation, resource sharing, and knowledge construction.

Intelligent tutoring systems, virtual laboratories, and feedback mechanisms that capture rich information about student performance and help students transfer their learning to new situations.

Mobile devices for accessing and inputting data during field-based investigations.

(Lombardi, 2007, p. 7)

It is all very well discussing what authentic learning is but the key is not to change the learning environment unless it enables students to perform better and enjoy their studies more. Therefore it is important to consider what effective learning is and whether authentic learning is effective for the student.

Lombardi (2007) states, “to be competitive in a global job market, today’s students must become comfortable with the complexities of ill-defined real-world problems. The greater their exposure to authentic disciplinary communities, the better prepared they will be ‘to deal with ambiguity’ and put into practice the kind of ‘higher order analysis and complex communication’ required of them as professionals” (p. 10). This implies that if a student is to do well in the job market the sooner they are exposed to authentic learning methods the better able they are likely to be in a working environment. However, if traditional assessment tools are used in higher education, authentic learning techniques in the classroom may help employability skills, but will they help the student to pass traditional style exams?

Herrington (2006) asserts, “authentic learning designs have the potential to improve student engagement and educational outcomes” (p. 1). This statement directly supports what this study is trying to test and suggests that authentic learning can improve assessment success. Herrington also argues that online technologies are key to the design and creation of innovative authentic learning environments and that tasks focusing on authentic activities are highly important. He also declares that the investigation of the effectiveness of authentic learning environments needs a comprehensive approach. In his article he states, “authentic learning environments […] are effective in promoting higher order learning […] but are only rarely used in higher education courses” (p. 1). In this paper, he also touches on the foundations of the concept of authentic learning in higher education being based on research into apprenticeships and their characteristics which were critical to success. “Brown et al. (1989) argued that meaningful learning will only take place if it is embedded in the social and physical context within which it will be used” (p. 1). He also utilises the ten characteristics of authentic learning as mentioned in the article by Lombardi (2007) and concludes that “the most successful learning environments employing authentic tasks are student-oriented, offering education as a process rather than a product […] providing cognitive realism,” (p. 4). Therefore a lot of his findings and comments agree to those of Lombardi.

To summarise the thinking on authentic activities, they need to reflect the real world, be problems that take time to solve, employing collective work, reflection, different resources, form part of a major task but not have one unique solution. They need to help employability skills but care also needs to be taken when designing them to ensure that they practise the skills necessary to be successful in passing assessments and motivate students to persevere with the subject in hand. These considerations have been built into the changes brought into the activities used in the Finance module as discussed in the next section.

As Finance is only part of the overall module, it was decided to supplement learning by changing teaching styles used in seminars by firstly introducing a scenario applying the subject matter learnt in lectures to a business situation involving decision-making about a project investment. This required students to produce their calculations in an Excel spreadsheet and present the justification of their choice of project as if in a board meeting using the techniques taught in the lecture. This activity was designed to reflect real world activities as would be used in the work place, required time to work through it, involved group work by the class splitting into small groups to carry out the calculations and present their findings and the use of different resources (spreadsheets, calculations, PowerPoint slides, technical knowledge of the tools to use and practical business considerations). It also required some reflection in order to justify the decision made in the presentation and different skills to be successful in putting the answer together. In addition, the activity was designed so that did not have one unique answer. This meant that the whole process covered a large number of the elements listed in the previous section which are deemed necessary for an activity to be seen as authentic.

Mini case studies were also used in seminars, covering a variety of business situations requiring finance. These described the type of business, the management structure and the reasons they required finance. They incorporated pictures and comments from managers about the scenario to tie into different learning styles as indicated in the work of Fleming (2001) discussed earlier. These provide a simple summary, a variety of scenarios and pictures of the business and helps the students to become more confident as it shows how a little bit of knowledge can help them provide suitable advice on sources of finance for businesses whereas the traditional exercises can leave the students overwhelmed and struggling to understand the technical material. This then fits into the element of authentic tasks where activities need to be built up into a major task as these mini scenarios are practice for the skills required in the decision-making exercise required in the task described in the paragraph above.

Further enhancements to this module involved linking the teaching on the Financial Accounting part of the course to that of the Finance element. In the Financial Accounting part of the module a particular company’s financial statements are used to apply the principles of the combined code and interpretations of accounts. The same set of accounts was used in the delivery of the Finance element of the course to extend learning and application of knowledge by checking the understanding of sources of finance by reviewing the sources currently used by the company being reviewed in the Financial Accounting part of the course and identifying potential future opportunities for sources of finance based on the company's current financial status. Again this supports the piecing together of activities to enhance coherence (Herrington, 2006), uses different resources and real world information whilst at the same time helping the student to practise activities that will be tested in the final assessment for the subject.

Feedback was obtained from the Financial Accounting tutor about their thoughts on using more practical case studies for the Finance element alongside the traditional style questions and extending the use of the financial statements to the Finance part of the course. The tutor thought that this was particularly useful to link and relate the separate parts of the course together and also for the weaker students it should build their confidence by introducing practical scenarios to show the variety of companies which can be considered and that although the lecture can make the topic seem very technical a lot of common sense can enable sensible suggestions and easy use of knowledge by students.

On the basis of the changes to the teaching tools used in the classroom, the assessment has also been changed from a formal written three hour exam for the subject with numerical and written questions across the three parts of the syllabus to a case study based on a company scenario involving coursework producing a three thousand word analysis of the scenario using the three discipline areas of the subject. This is produced as a report as if required by a business with written analysis and supporting calculations to back up narrative and is much more conducive to the type of exercise which would be carried out in business.

Therefore the changes to the Finance module above fulfil the criteria provided in the relevant literature to provide an authentic learning environment for students. The question remains however whether this has been worthwhile in terms of improving pass rates and student enjoyment.

The new, more ‘authentic’ methods of delivery and assessment were introduced at the start of the academic year 2013/14 to the MBA Finance module. The aim of this journal article is to assess whether authentic learning is effective in terms of whether it has a positive impact on pass rates and whether students enjoy the learning experience more as a result of these learning methods?

Although it is not possible to measure the changes on the same cohort of students (as no students repeated the module from 2011/12 to 2014/15) it can generally be accepted that overall pass rates for the same subject from one academic year to the next and student evaluation form scores and comments can be a close measure to ascertain whether the more authentic learning methods have boosted exam success and enjoyment.

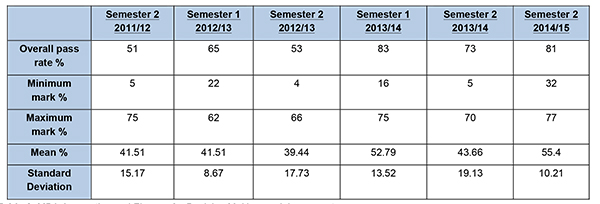

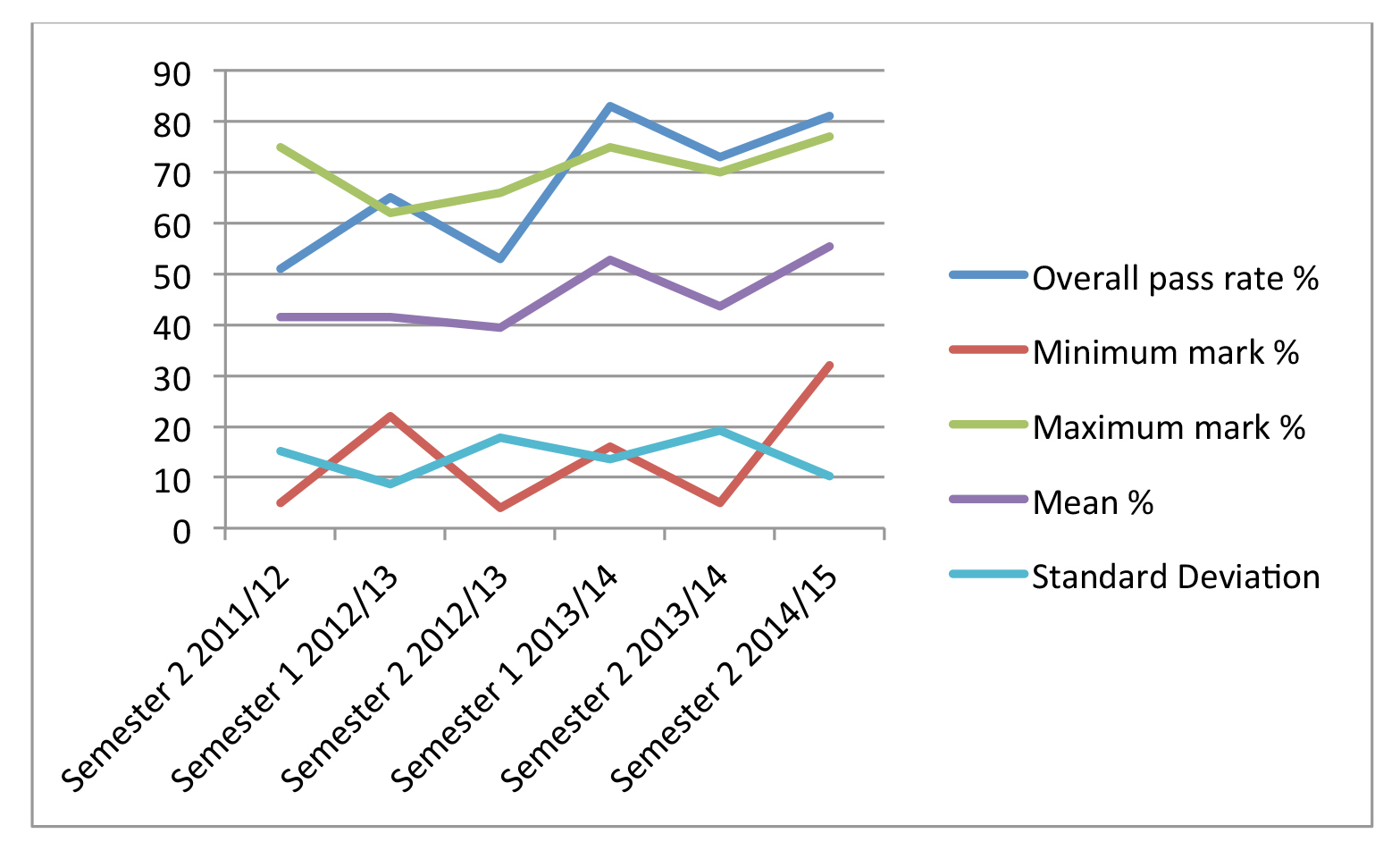

The module is taught to different cohorts for each semester of the academic year. Table 2 below summarises the subjects pass rates for the three semesters before the changes and the three semesters when the changes have first been introduced. As can be clearly seen in table 2 below, the pass rates with the changes (from semester 1 2013/14) are higher than the pass rates before. The pass rates before the changes range from 51% to 65% and after the changes range from 73% to 83%. If the spread of the results is analysed, the minimum and average marks are not that much different between the two teaching styles, however the maximum marks have been more consistently achieving above 70%. Initially it was thought that the type of authentic learning introduced would be of greatest benefit to the students struggling with the subject so it is interesting that the highest marks (and therefore one can assume the most able students) seem to have done better as a result of the changes and the average and lower end has not seen much uplift. Overall, the data suggests that authentic learning has had a positive impact on the success of students studying this module and could be beneficial to improving assessment success. The trends discussed are more visible in the graph in table 3 which emphasises the increase in the overall pass rate over the period and the improvement in the maximum mark.

Table 2: MBA Accounting and Finance for Decision Making module pass rates

Table 3: Graph of MBA Accounting and Finance for Decision Making module pass rates

Alongside pass rates, this journal article also wants to establish whether authentic learning is more enjoyable for students as this was an area of weakness for this subject and also a happy student should hopefully be more motivated to study.

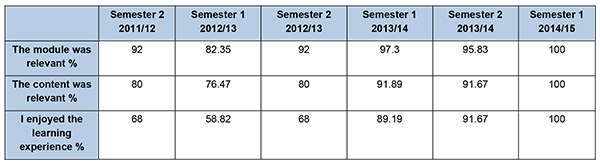

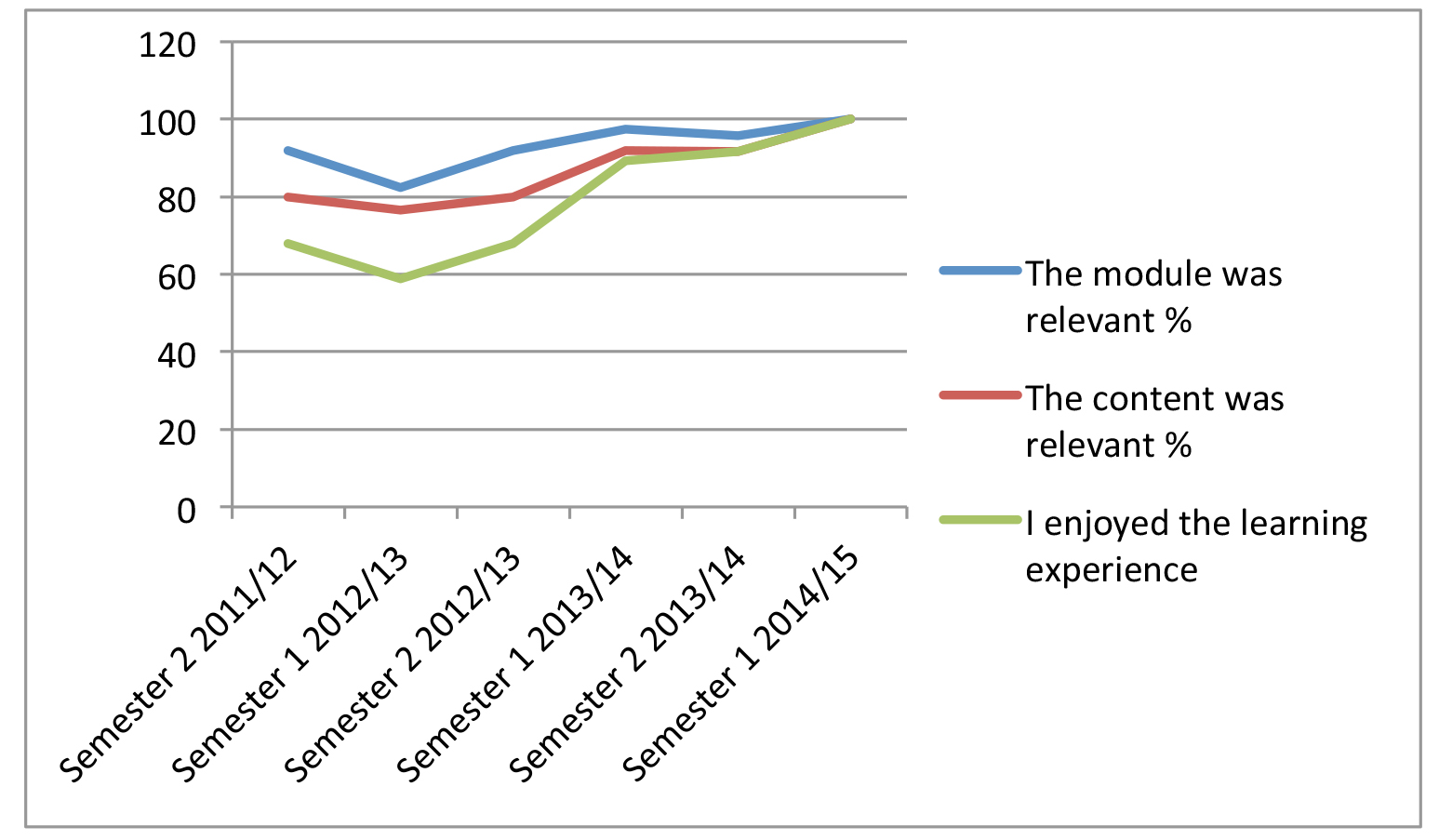

The aim of this paper was to review the module evaluation forms for the same period as the exam results. From the module evaluation forms, the questions relevant to the enjoyment of authentic learning were reviewed and the scores that they averaged across the cohort. These questions were: ‘was the module relevant’, ‘was the content relevant’ and ‘did the student enjoy the learning experience’. The results are summarised in table 4. Improvements in the scores from semester 2 2011/12 to semester 1 in the academic year 2013/14 can be seen for all the questions but particularly the enjoyment of the module seems to have improved significantly from the 58-68% range prior to the changes to 89-100% in the semesters after the changes. Again this is much more noticeable when seen in table 5 where the graph highlights the increase in student enjoyment of the learning experience once the teaching and assessment methods have been changed.

Table 4: MBA Accounting and Finance for Decision Making module evaluation scores

Table 5: Graph of MBA Accounting and Finance for Decision Making module evaluation scores

In addition to the scores illustrating student satisfaction with the module, any comments made on the forms pre and post the changes were reviewed by myself when relevant to the introduction of authentic learning. Relevant, qualitative, free text comments from the module evaluation forms pre the changes included “more real examples needed” and also “more problem-solving activity required.” Post changes comments include “useful and practical, great tutorial experience”, “lectures were made interesting and I enjoyed the learning experience” and “the module is very relevant and has helped a lot to enhance my knowledge”.

This study has focused on just one part of a module where attempts have been made to introduce authentic learning techniques. The same cohort could not be measured pre and post the changes, however the evidence suggests that the introduction of authentic learning techniques and assessment methods can not only make student learning more effective in terms of better pass rates but also that students enjoy the learning experience more. The findings therefore bode well for the further use of authentic learning techniques in future teaching and learning activities and also support the findings and suggestions of the literature reviewed as part of this article. The changes to the teaching methods continue to be used and the assessment style has also continued to use a case study based on a real life scenario across the whole of the module with a continued uplift in pass rates and student satisfaction.